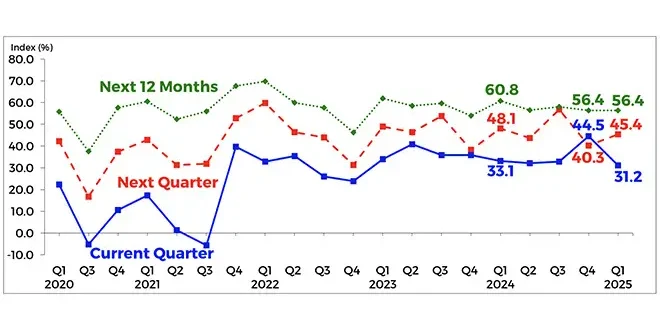

Business sentiment in the Philippines was less optimistic in Q1 2025, with the overall confidence index (CI) dropping to 31.2 percent from 44.5 percent in Q4 2024.

This decline reflects a combination of a decreased percentage of optimists and an increased percentage of pessimists.

The firms’ less optimistic outlook for Q1 2025 was primarily driven by concerns regarding: (a) the post-holiday decline in demand for goods and services, along with a slowdown in business activities, and (b) a potential resurgence of inflationary pressures.

For Q2 2025, the country’s business sentiment became more upbeat, with the overall CI increasing to 45.4 percent from 40.3 percent in the Q4 2024 survey results. For the next 12 months, the business outlook remained buoyant, with the overall CI holding steady at 56.4 percent, unchanged from the Q4 2024 survey round.

The business sentiment for Q1 2025 was generally less optimistic across all sectors, except for the construction sector, whose optimism was little changed.

Business confidence across all types of trading firms was generally less optimistic in Q1 2025. The CIs of exporters, dual-activity firms (engaged in both importing and exporting), and domestic-oriented firms were lower compared with the Q4 2024 survey results, while that of importers was little changed.

The average capacity utilization for both the industry and construction sectors in Q1 2025 decreased to 71.4 percent from 73.9 percent in Q4 2024.

Firms expect tight financial condition and credit access in Q1 2025. Firms expect tighter cash or liquidity positions in Q1 2025 as the financial condition index became more negative.

Moreover, businesses anticipate that access to credit to turn tight in Q1 2025, as the credit access index (CAI) reverted to the negative territory.

Businesses anticipate a weaker peso and higher interest rates in the first half of 2025. Firms expect that the peso may depreciate against the US dollar in Q1 and Q2 2025 but may appreciate over the next 12 months. Meanwhile, businesses expect that peso borrowing rates may rise during these periods.

Businesses expect higher inflation rate in Q1 2025, Q2 2025, and the next 12 months. Businesses anticipate that the inflation rate may rise in Q1 and Q2 2025, as well as over the next 12 months. Moreover, stronger inflation expectations may be observed in all reference periods, as the percentage of firms expecting higher inflation increased vis-à-vis the Q4 2024 survey results.

Firms also expect that the inflation rate may average 3.2 percent in Q1 2025, 3.3 percent in Q2 2025, and 3.4 percent over the next 12 months.

All of these inflation expectations fall within the National Government’s inflation target range of 2.0 – 4.0 percent for 2025-2026.