It has been an ongoing discussion since last August as to when the US economy will enter a recession, though it seems it will take something big to knockout the world’s largest economy.

It has been an ongoing discussion since last August as to when the US economy will enter a recession, though it seems it will take something big to knockout the world’s largest economy.

Just back in August and September last year, a pretty large number of economists expected the US economy to enter a recession by the end of this year or in 2020. The latest surveys among economists covering the US economy indicate that the expected entry in the recession has moved out to 2021. Perhaps it will never come, but there are other risks that could be bigger.

The US household debt was equal to 99 pct. of GDP when the global financial crisis hit the world about 10 years ago, now the household debt accounts for 77 pct. of GDP. It does not mean that all American families have generally become more wealthy, and the biggest reason for the improvement is simply because the total GDP has grown over the past decade.

However, this does not change the fact that on a relative basis, American households have generally reduced debt, thus becoming less vulnerable to an economic crisis.

Property prices have also risen in the US, and even in an interest-rate environment, the 30-year interest rate on house financing in 2018 rose to the highest level in more than seven years. It’s important to note that the price increases were due to demand and economic growth, unlike in Europe where housing prices have mainly gone up because mortgage rate on housing financing is close to zero pct. in some countries.

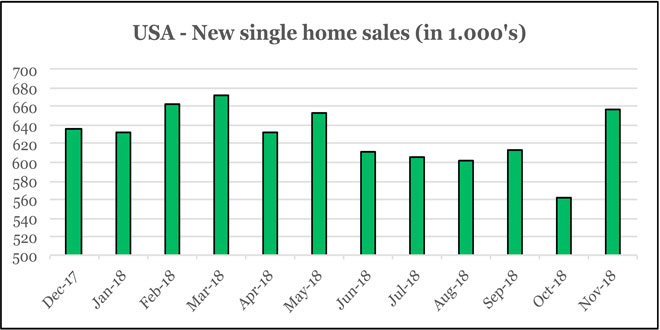

In the US, however, house prices have increased more than wages over the past several years. It leads me to believe that the pace of price increases will flatten out in the next few years, but there are no signs of a crisis so far. However, the slump in the sale of new homes in October (graphic one) caused a moment of concern, but it’s back on track, though I will give it some attention.

These are examples why I argue that US households have become more economically robust to forego a crisis and nothing currently points towards a recession. Still, private consumption accounts for 70 pct. of the total US GDP, so a stable outlook for the households also constitutes a stability for the US economy.

The chairman of the US central bank (Fed), Jay Powell, has recently given his testimonies to the Congress in Washington DC. Fed’s assessments were quite interesting, as it appears that neither is the central bank very concerned about the US economy. The biggest challenges for the American economy are the global headaches such as the Brexit and possibly a continuing trade dispute with China.

Overall, Fed notes that the economic growth environment is not quite as favourable as it was a few months ago, though on the other hand, not worse than just a change.

On the topics of household income, Fed also mentions that wage increases in the low-paid segments remain on the rise, and the labour market still has room for growth.

Fed points out that in the rural areas, the US has a 78 pct. job participating rate among people aged 25 to 54, this climbs even higher to over 80 pct. in urban districts, proving therefore there is still a free labour force that can contribute to economic growth.

Overall, I judge the various assessments from Fed that their greatest concern about growth are global headwinds, which could cause a negative impact on the country’s corporate sector. I agree that businesses can be hit more than households, which will certainly create a negative impact on GDP growth, but it remains well-off a recession.

The development in inflation (graphic two) is a natural focus of the central bank, where the primary reason for the drop in inflation originates from energy prices. Underlying, the core inflation does not move lower, but is stable at around 2.2 pct. We have learned from Fed that they are not worried about inflation, so they stay-put on interest rates. But Fed has made another interesting monetary policy comment – the central bank plans to have a bigger balance sheet in the future than what they had before the global financial crisis.

I agree that USA is heading towards lower economic growth rates, but not enough to fall into a recession. It will have implications, such as a negative contribution to the expected return from US stocks, which could very well be 5 pct. annually in the years to come, though better than a loss in a recession.

The big difference from before the global financial crisis is that many governments in advanced economies have increased debt largely in order to keep the GDP growth up. This also applies to the US government, which increased the sovereign debt enormously during the global financial crisis, followed by a second round in connection with last year’s tax cuts.

My view is that a debt crisis is more likely to happen at some point, rather than an economic crisis. A debt crisis will of course be a disaster for economic growth, but it does matter where the problems arise – a debt crisis or economic crisis.

Concerning the US government debt, a crisis develops when investors consider the sovereign debt has become too high – this may well happen one day, though it will take a long time.

The coming lower growth means that some companies will be pressured on the earnings, which usually causes debt-ridden companies to succumb. Models using data from before the financial crisis will probably soon predict financing problems among debt-loaded corporations.

Though here, Fed’s bigger balance sheet (as well as the very large balance sheets of other central banks) plays a role. Simply because the continued abundant liquidity means that companies with weak equity still find it easier to get funding than before the global financial crisis.

Obviously, I do not belong to the camp that believes in a recession in the US economy. Instead, I spend my time assessing how much debt makes corporations with low equity vulnerable. But even concerning these investments, the risk is smaller for the investor than a model might indicate how the risk is expected to be ahead of a slowdown in economic growth.